Case 01 · Food manufacturing

CSBFP · $500,000

Small-batch tofu producer, Greater Toronto Area

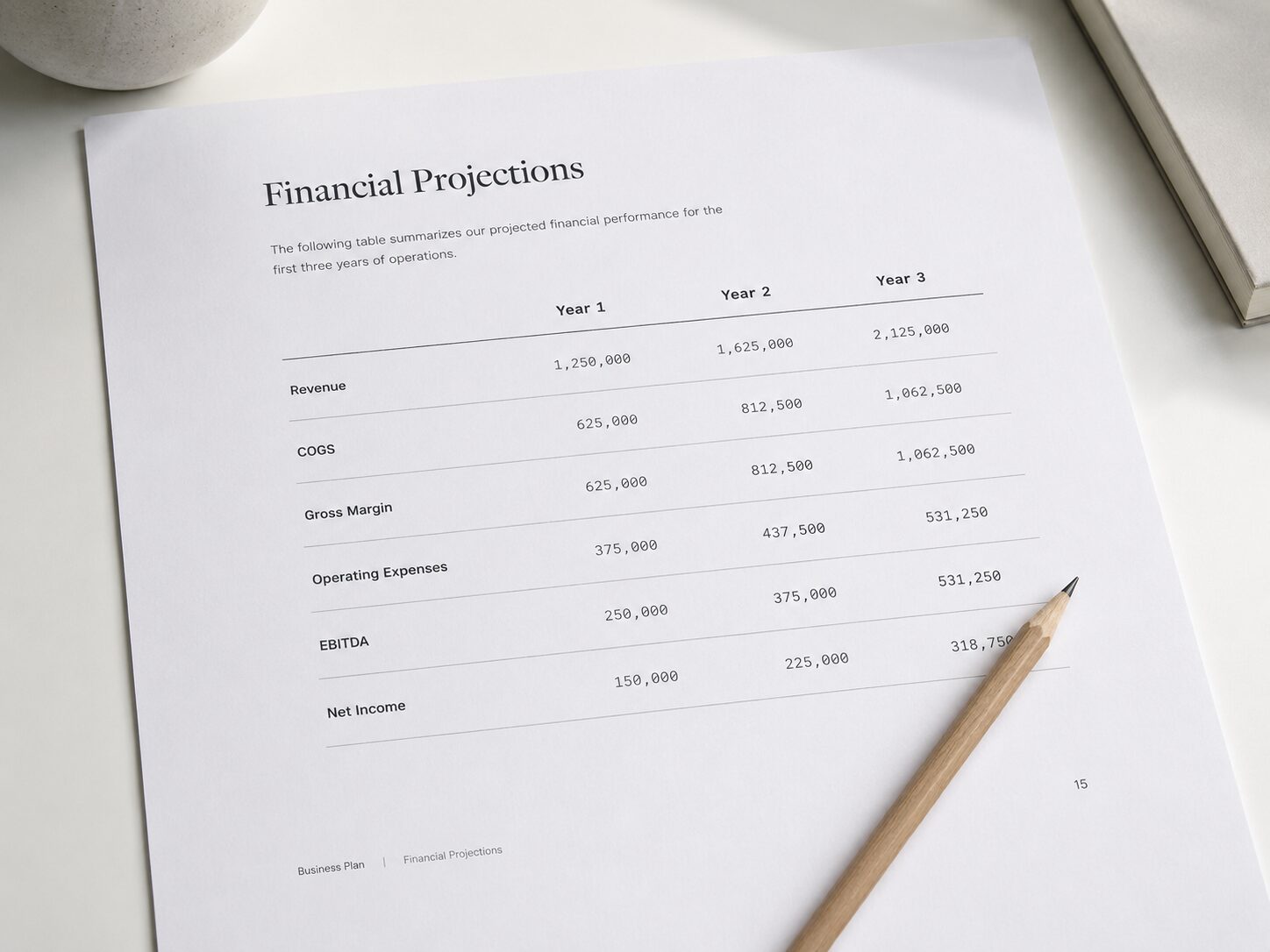

The client arrived with strong product-market fit and a growing wholesale customer base — but the underwriting fundamentals weren't documented. No income statement projections, no worker-hour assumptions tied to production capacity, no defined target loan amount, and no use-of-funds breakdown in the CSBFP-expected eligible-asset format.

We scoped the engagement around:

- Right-sizing the loan request against actual equipment and working-capital needs

- Building hour-level workforce projections tied to production throughput

- Validating revenue and gross-margin assumptions against comparable Canadian specialty food processors

- Drafting a use-of-funds line item that mapped to CSBFP's eligible-asset categories (equipment, leasehold improvements)

Outcome

Plan approved after one lender review round — no requested rewrites.